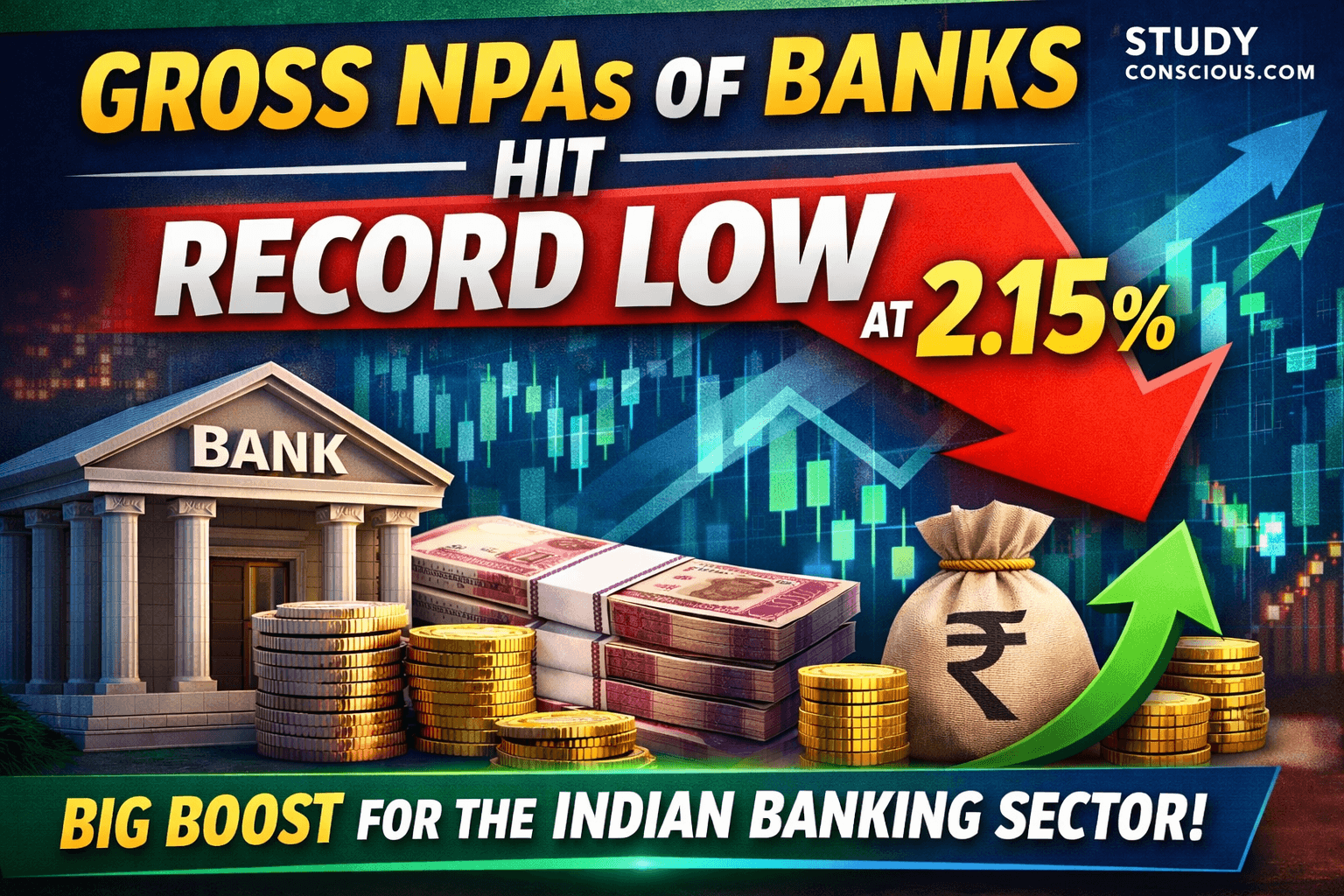

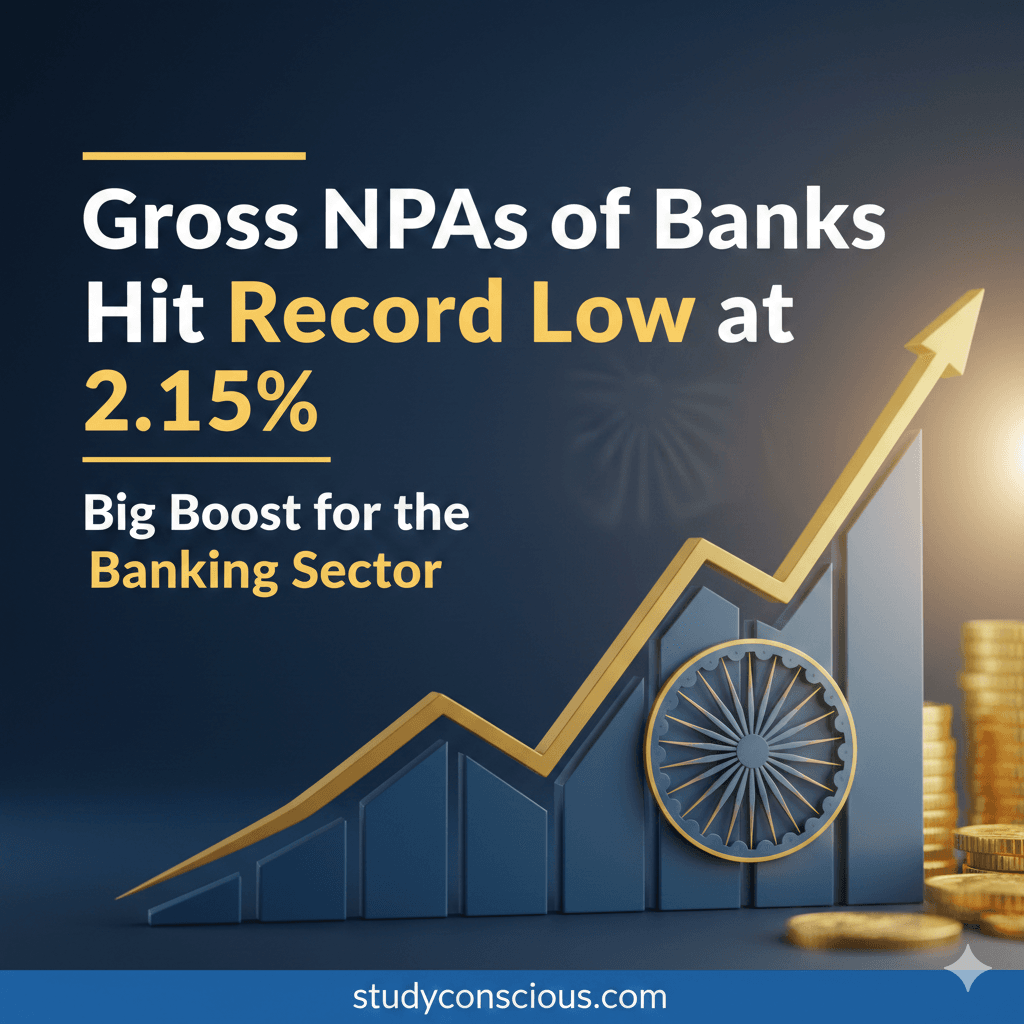

India’s banking sector has achieved a major milestone as Gross Non-Performing Assets (NPAs) of banks have fallen to a historic low of 2.15%. This is the lowest level in many years and marks a strong turnaround for the Indian banking system.

Why Have NPAs Declined?

The fall in NPAs is not accidental. It is the result of multiple structural and cyclical factors working together.

1. Better Credit Discipline

Banks have become far more cautious in lending after the bad-loan crisis of the last decade.

- Stricter due diligence

- Focus on cash flows instead of just collateral

- Reduced exposure to risky corporate lending

2. Faster Resolution of Stressed Assets

The Insolvency and Bankruptcy Code (IBC) has improved recovery timelines.

- Large corporate NPAs were resolved or written off

- One-time settlements cleared legacy stress

- Recovery rates improved compared to earlier regimes

3. Stronger Economic Recovery

Post-pandemic economic growth improved borrowers’ repayment capacity.

- Higher corporate profits

- Improved MSME cash flows

- Better employment conditions

4. Lower Slippages

Fresh NPAs have reduced sharply.

- Retail loans (home, auto, personal) are performing well

- Digital monitoring and early warning systems are catching stress early

5. Government and RBI Support

- Capital infusion into public sector banks

- Targeted restructuring schemes

- Timely regulatory intervention helped prevent stress from snowballing

What Does This Record Low Mean for Banks?

Stronger Balance Sheets

Lower NPAs mean less money stuck in bad loans. Banks now have:

- Lower provisioning burden

- Higher net profits

- Improved capital adequacy

Higher Lending Capacity

With cleaner books, banks can:

- Lend more to businesses and consumers

- Support infrastructure and MSME growth

- Compete better on interest rates

Improved Investor Confidence

Banking stocks benefit directly from better asset quality.

- Lower risk perception

- Higher valuations

- More stable earnings outlook

Impact on the Economy

A healthier banking system strengthens the entire economy.

Credit Growth Picks Up

- More loans to industries and MSMEs

- Better support for housing and consumption

Lower Systemic Risk

- Reduced chances of banking stress or bailouts

- Greater financial stability

Faster Economic Growth

Banks act as growth engines when balance sheets are strong.

What It Means for Investors

For Equity Investors

- Banking stocks become more attractive

- Improved ROA and ROE

- Lower downside risk from surprise NPAs

For Bond and Debt Investors

- Lower default risk

- Improved confidence in bank-issued instruments

Is This Improvement Sustainable in the Long Run?

Reasons for Optimism

- Structural reforms like IBC are permanent

- Better risk management practices are now embedded

- Retail loan performance remains strong

Risks to Watch

- Rapid credit growth could dilute underwriting standards

- Stress may emerge if interest rates remain high

- Certain segments like unsecured retail and MSMEs need close monitoring

Overall Assessment

The current improvement appears largely sustainable, provided banks:

- Maintain lending discipline

- Monitor emerging stress early

- Avoid aggressive risk-taking during credit booms

Bottom Line

The decline in NPAs to record lows signals a structurally stronger banking system.

For banks, it means profitability and growth.

For the economy, it means stability and expansion.

For investors, it reduces risk and improves long-term visibility.

Our Recent Blogs:

India Vs Pakistan Cricket Match Scheduled for February 15, 2026

The US will include India in the Pax Silica initiative, which aims to challenge China!